Why Investment in Defence, Aerospace and Security is Good for the Whole of the UK

Chancellor Philip Hammond’s autumn budget statement has laid out the government’s determination to shield the national economy from the effects of Britain’s anticipated departure from the EU.

Hidden inside the Autumn Statement – and not picked up by the subsequent media coverage – is the government’s Northern Powerhouse strategy, which will be followed up by a Midlands Strategy next year. Both are efforts to rebalance the national economy away from London and the South East, by diverting attention and resources on regions further north, home to 15 million people and consumers – one of Europe’s biggest economic regions.

Curiously, however, defence, aerospace, space and security industrial and services sectors are not mentioned as part of the Northern Powerhouse strategy, despite the presence of a number of hi-tech defence firms in the region. And with officials indicating that the update to the 2012 white paper, National Security Through Technology, will not materially change the Ministry of Defence’s (MoD) policy on an open defence sector that allows all global players to participate in the UK and have access to the £16-billion annual equipment budget, it seems that the government is intent on closing its eyes to the broader benefits of the UK defence, aerospace and security sectors as part of a national industrial strategy – both in the short and long term.

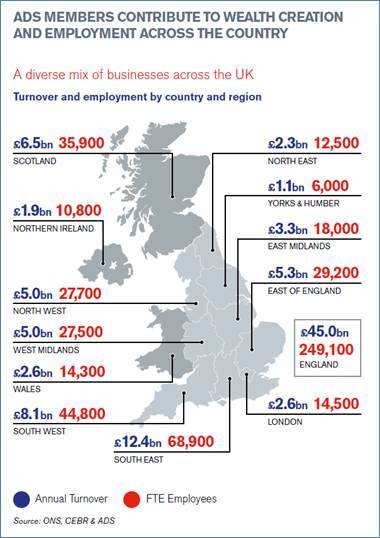

A quick scan of the website of ADS, the umbrella organisation for this sector, shows this is an industry providing £35-billion worth of exports, supporting 340,000 direct jobs and 10,400 apprenticeships. Of the organisation’s 900 members, almost 75% of their direct employment in its four sectors – defence, aerospace, space and security – is outside London and the South East, including around 45,000 direct jobs in each of the South West, Midlands and Northern Powerhouse regions (see Figure 1 below for full regional breakdown of turnover and employment).

Moreover, these are growing sectors. Space, for example is one of the fastest growing sectors today, doubling to $330 billion over the last decade. The UK Space Agency is aiming to grow the UK space economy from £11 billion today to £40 billion by 2030 and to grow employment in the sector from 34,000 today to create 100,000 by 2030 – a 300% increase. Similarly, the aerospace sector will be worth over £4 trillion between now and 2030, while the UK’s security sector is seeing year-on-year growth, particularly in cyber security, which represents 45% of the export market.

Sectoral-based initiatives through existing industrial strategies – such as the aerospace growth partnership, defence growth partnership and space growth partnership – are also proving a valuable way to deliver local growth for local industry. Indeed, part of what makes the Aerospace Growth Partnership so successful is that 70–80% of the companies benefiting from its programmes are located outside London and the South East.

The chancellor’s broader commitment to R&D and to innovation is certainly good news for the sector as well, adding to the MoD’s existing Defence Innovation Initiative. The chancellor proposed a three-pronged approach:

- An extra £2 billion in R&D funding (+£425 million in 2017/18, +£820 million in 2018/19, +£1.5 billion in 2019/20) bring a total of £4.7 billion by 2020.

- An industrial strategy fund built on the model of the US Defense Advanced Research Projects Agency and managed by Innovate UK.

- An injection of £400 million into the British Business Bank in order to unlock a potential £1-billion financing fund through venture capital.

The last of these initiatives should also help small to medium enterprises scale up, which is proving particularly problematic in the cyber security arena.

However, the biggest challenge to the future of the UK’s defence and aerospace businesses is the lack of national ambition in terms of future platforms. According to Britain’s Department for International Trade, around 88% of UK defence exports are in aerospace, compared to the 68% of global average for comparable countries. Despite this, the MoD announced a bonanza in terms of aerospace procurement from the US in the 2015 Strategic Defence and Security Review – 24 Joint Strike Fighter aircraft, nine P-8 aircraft and over 20 Protector remotely piloted air systems. This leaves very few future UK air platform programmes in the inventory for future exports over the next fifteen years and while the UK has a ship-building strategy (at some considerable cost), the MoD’s approach to land systems looks to be following the air sector.

While the chancellor has focused on supporting infrastructure projects in his Autumn Statement, we should not underestimate – at a time of austerity – what a flagship space or aerospace programme might mean both for industry today but also in terms of inspiring the next generation of STEM (Science, Technology, Engineering and Mathematics) professionals. UK industry has invested in Reaction Engine’s SABRE programme and the UK Space Agency’s commitment to UK space launch capabilities is a start but we need to go much further.

The prime minister has been clear in her speech to the Confederation of British Industry that the government will not prop up failing industries. And certainly, the British defence industry has been guilty of waiting for government subsidies in the past; it needs to invest more of its own money in R&D to generate future products, create a suite of platforms that are affordable to a wider range of armed forces and diversify into the commercial sector in order to reduce the costs. Defence, however, still has many characteristics of a monopsony (overseas customers will not buy platforms if the British armed forces do not use them first) and defence exports and training are still used by allies and partners as a means to enhance their broader relationship with the UK.

Therefore, defence engagement opportunities will diminish if all our defence products are subcomponents on a US or German platform. Moreover, operational adaptability and rapid reconstitution may be difficult if there is no indigenous industrial base capable of meeting urgent operational requirements.

In summary, defence, aerospace, space and security are growing sectors and should be very much at the heart of the UK’s industrial strategy. The MoD should look to use its £36-billion/year budget to support UK industry – particularly given that it is one of the few ring-fenced departments. Perhaps it should also consider jointly developing platforms with other government departments as well as allies and partners overseas.

More broadly, the government needs to urgently consider the long-term prospects for UK exports given the lack of platforms in the forward defence equipment plan; but a flagship space or aerospace programme would inspire a new generation and provide a valuable boost to the national skills base. Perhaps there was too little space for this in the Autumn Statement. But there should be plenty of space for such initiatives in future government plans.